Online commerce transactions are the essential fuel that drives the Global Networked Economy. Digital business growth experienced an economic uplift as a consequence of the economic challenges that accompanied the global health crisis brought on by the COVID-19 pandemic.

At the same time, the digital transformation of consumer transactions contributed to even greater upward momentum. Even as more legacy retailers shifted to eCommerce, the last 24 months have been the most difficult time for mid-market retailers as they recover from the pandemic disruption.

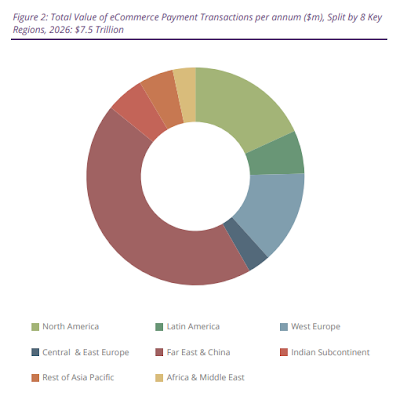

Global eCommerce Market Development

According to the latest market study by Juniper Research, the value of global eCommerce payment transactions will exceed $7.5 trillion by 2026 -- that's up from $4.9 trillion in 2021.

This growth rate of 55 percent over the next five years will be driven by retailers offering compelling omnichannel retail experiences that increase user eCommerce spending.

Omnichannel retail is a model that provides end-users with the ability to access retail services, including sales and customer support, via multiple online channels.

Juniper analysts predict that these combined channels -- including online, mobile, and physical retail locations -- will be instrumental for future success. This is because users expect the same services to be available irrespective of the channel.

Juniper analysts predict that these combined channels -- including online, mobile, and physical retail locations -- will be instrumental for future success. This is because users expect the same services to be available irrespective of the channel.

Additionally, Juniper found that there are increasing appetites for new payment methods within eCommerce checkouts, including open banking-facilitated payments and digital wallet one-click checkout buttons.

According to the Juniper assessment, it now recommends that merchants ensure online payment options match changing consumer expectations for ease of use, or they will be rapidly left behind.

The research found that by 2026, China will account for over 37 percent of global eCommerce payments by transaction value, owing to its established and extensive eCommerce and payments landscape that provides greater convenience for users via easily accessible alternative payment methods.

Additionally, Juniper recommends prioritizing digital wallets, open banking‑facilitated payments and cryptocurrencies to emulate the eCommerce success experienced in China.

Additionally, Juniper recommends prioritizing digital wallets, open banking‑facilitated payments and cryptocurrencies to emulate the eCommerce success experienced in China.

To do so, they recommend that platform providers partner with specialists in these specific emerging payment areas keep pace with changing merchant expectations around acceptance types.

Outlook for eCommerce Applications Growth

Looking forward, Juniper now forecasts that physical goods will account for 82 percent of the global eCommerce payments transaction value by 2026.

Outlook for eCommerce Applications Growth

Looking forward, Juniper now forecasts that physical goods will account for 82 percent of the global eCommerce payments transaction value by 2026.

Their analysts urge payment providers to support BNPL -- an alternative payment method that integrates fixed installment plans and flexible credit in eCommerce checkout options -- to capitalize on the continuing growth.

That said, I believe digital payment options will continue to evolve as more progressive retail organizations seek new ways to attract and retain the diverse demographic segments of shoppers that have very different needs for their preferred online retail user experience.