Today's electronic commerce is an engine of the world’s Global Networked Economy. It experienced an uplift in 2020 and 2021 as a result of the disruption created by the COVID-19 pandemic. Meanwhile, business and consumer online transactions contributed to significantly greater growth momentum.

According to a survey by The Economist, brick-and-mortar retailers have shifted rapidly to eCommerce. However, many traditional retailers are still recovering from the backlash of the ongoing pandemic.

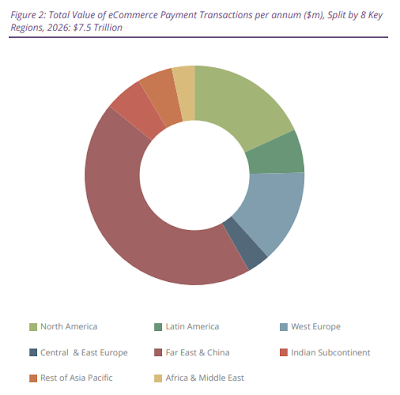

eCommerce Payment Market Development

Juniper Research's latest market study has found the volume of global eCommerce transactions made via OEM Pay will exceed 30.7 billion by 2026 -- that's rising from 4.7 billion transactions in 2022.

This outstanding market growth of 550 percent will be driven by rapidly increasing customer demands of frictionless retail checkout experiences across multiple eCommerce channels.

Juniper's new research findings predicted that OEM Pays will benefit, as alternative payment methods like Buy Now Pay Later (BNPL) are becoming progressively mainstream in the retail sector.

eCommerce users are increasingly demanding low-friction checkout processes -- which OEM Pays, including Apple Pay and Google Pay -- are well placed to offer. Juniper's analysts recommend that merchants work closely with payment platforms to increase acceptance of digital wallets, or risk losing market share to competitors.

According to the Juniper assessment, eCommerce OEM Pay transactions will grow by 516 percent between 2022 and 2026 in Western Europe. They identified the region as a leader in the growth of digital wallet use over eCommerce channels, further driving the development of OEM Pay transactions.

Regardless, the Juniper market study findings now indicate that growth outside of Western Europe will lag, as mobile contactless payments are yet to gain significant traction in other key global markets.

The research also identified an increase in consumer awareness for the enhanced financial transaction security measures offered by OEM Pay services, such as biometrics and tokenization.

These features were found to drive mainstream adoption. Juniper forecast a growth of 63 percent for OEM Pay transaction volume globally in 2022, largely driven by a greater consumer acceptance and trust of mobile payments throughout the pandemic period.

Outlook for eCommerce Payment Applications Growth

Juniper analyst's research suggested that eCommerce merchants should capitalize on this now by ensuring that security processes are consistently robust across all retail payment methods.

That said, I believe all channels -- including online, mobile, and physical retail locations -- will be instrumental for future commercial success. This is because retailer customers expect the same services to be available irrespective of the channel type.

Additionally, there is increasing demand for new payment methods within eCommerce checkouts, including Open Banking-facilitated payments and digital wallet one-click rapid checkout buttons.