Building on significant advances in disruptive mobile app technology, ride-sharing services have emerged to become a popular means of urban mobility. This is unsurprising given the advantages of ride-sharing options over traditional transport modes, such as buses and more expensive taxis.

Innovative ride-sharing platforms enable app users to customize their journeys according to real-time phenomena, such as nearby traffic conditions, time of day, and rider demand. However, this is not to say that ride-sharing services are perfect.

The popularity of ride-sharing has resulted in some additional traffic congestion in major cities already struggling to control this issue, while the widespread disruption caused by the pandemic affected most stakeholders within the local transportation value chain.

Ride-Sharing App Market Development

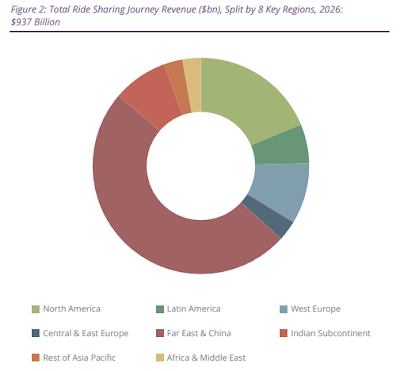

According to the latest worldwide market study by Juniper Research, ride-sharing spending by consumers globally will exceed $937 billion by 2026 -- that's comparable to 50 times the combined annual revenue of Transport for London, New York City’s MTA, and the Beijing Metro in 2021.

This spending on ride-sharing represents an increase from $147 billion in 2021 and rapid total growth of 537 percent over the next 5 years. Regardless of attempts by some city government officials and their local legacy taxi company owner complaints, they won't stop competition and innovation.

The concept of ride-sharing involves users accessing single-occupancy and shared carpool-style services provided by private drivers operating their own vehicles -- coordinated by mobile-enabled app platforms such as Lyft and Uber.

Juniper analysts identified people in the U.S. and China markets as leading global spend on ride-sharing services -- accounting for 65 percent of market value in 2026.

The study findings highlighted future government initiatives to reduce private vehicle usage in cities, allied with a strong pandemic recovery, as key to these countries’ positions as market leaders.