Digital identity combined with security, privacy, and data management are interrelated requirements, and in some cases, they are indistinct. In the U.S. market, digital identity is described as the online persona of a human subject.

The term "persona" means an individual who can present themselves in a variety of ways online. However, the definition varies between countries. This description is further complicated by the current multi-use ecosystem of digital identity.

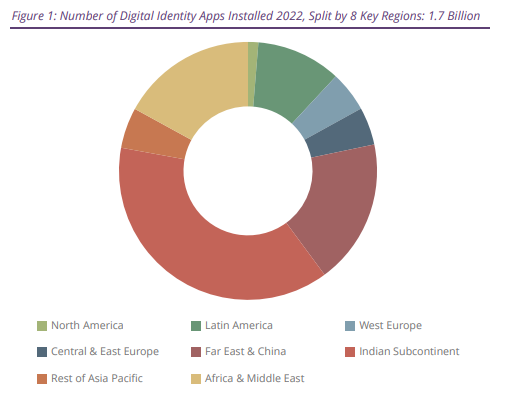

Digital Identity Market Development

According to the latest worldwide market study by Juniper Research, the number of digital identity applications in use will exceed 4.1 billion globally by 2027 -- that's rising from 2.3 billion in 2023.

This represents a growth of 82 percent over the next four years. The increase will be driven by the use of government-backed digital identities to replace physical identity documents as a source of verification for third-party apps, such as banking and financial services.

This trend will be critical, as businesses aim to reduce identity theft and meet increasingly stringent Know Your Customer (KYC) regulations imposed by governments via their compliance mandates.

Juniper's analysts also identified a move away from reliance on passwords for identity verification. These were replaced by biometric verification and Multi-factor Authentication (MFA) under a zero-trust model, where identities are authenticated continuously.

This advanced approach to the known challenges is more resistant to traditional online hacking methods, such as phishing, thereby helping to reduce the cybersecurity risk of data breaches.

One solution is the method known as Zero Trust, which will be delivered via Single Sign On (SSO), allowing online service users to access multiple accounts via a central, secured identity system.

The application of mobile subscriber identity is critical to SSO, with the total mobile devices using their phone number for SSO predicted to reach 2 billion in 2027 -- that's up from 922 million in 2023.

"Consumers are highly motivated by convenience; making a streamlining of user experience significant for attracting and retaining them. SSO can achieve this, while also appealing to security-conscious users," said Michael Greenwood, research analyst at Juniper Research.

The primary competition for dedicated digital identity applications will come from digital wallets, which offer payment functionality alongside a digital identity capability.

According to the Juniper assessment, in some U.S. states, digital driver's licenses held within Apple Wallets are fully recognized on a smartphone.

However, these digital wallets will struggle to monetize identity in the same way as they have payments, due to competition from government-run programs that may limit adoption.

Outlook for Digital Identity Applications Growth

Again, the common use of digital identity is the replacement of traditional physical forms of identity verification. This could be official government documents or some form of employee identification.

There are use cases in both the public and private sectors. The most common form of digital identity authentication is user names and associated passwords used to gain access to online services.

That said, the emerging and rapid growth of a distributed workforce model requires enterprise CIOs and CTOs to explore the most secure ways to protect remote-working employees and any corporate or personal data that they're able to access.

That requirement has created significant demand for comprehensive Digital Workspace solutions that enable an enterprise IT organization to deliver any software app, on any device, and at any location.